I first started using Discovery Vitality in 2008, when my work moved locations next door to a newly-built Virgin Active. Back then Vitality was R109, and to get “free” gym within that price was worth it alone. In addition, Vitality took a risk and let you get back a percentage of your spend at Pick n Pay; I think it was for healthy food only, and 25% across the board. All that to say, I made at least R400/m off Discovery, and loved it but… a lot has changed since then! It’s 16 years on now, and Discovery Vitality has become much smarter at plugging all the loopholes, and ironing out its pricing, rewards, and much else. This article below aims to help those who want to join Discovery Vitality for the first time, or, those who haven’t really kept up with the changes, and want to learn them for this current year.

The basics of Discovery Vitality

Essentially, without Vitality, you lose out on a ton of rewards within the Discovery ecosystem. In another article – mainly aimed at Discovery Miles and whether to join Discovery Bank – I outline just the tip of the iceberg, and here I aim to complement the info there, with this article focusing specifically on Discovery Vitality itself. Bear in mind I don’t intend on getting incredibly granular on everything within Discovery, but I will touch on various products/apps/ideas within each. If I was to get super detailed this article, and others on my website, would be just as big as Discovery’s website, so you may as well go there. I mainly want to give overviews, and caveats that will prevent you from wasting time only to give up half way.

The main premise of Vitality is that for a small fee each month (I pay R465/m for a small family, though it is tied to my name – i.e as the main member of Discovery Health it has to run through me) I get about 2-15 times back that fee in cash and rewards. If you are willing and able, it’s very possible to get about R5,000 back in cash each month, and if you choose rather to convert Discovery Miles into rewards (rather than cash) it can probably be up to about R8,000 or R9,000 per month. It’s complicated, but let’s dive in.

the ‘Spend to save’ paradox

Once you’ve paid your R465/month – or only R329 if you are a single member, sans a spouse, a child, etc – you immediately can qualify for some savings. Virgin Active gym was my first one 16 years back – saving 100% of the fees back then, but now it’s only 75%. I currently pay R273, instead of R1,000+/month. But the main reason is the whole “Vitality Active Rewards” represented in three rings. Vitality Exercise, Vitality Drive, and Vitality Money. With each of these “methods” or “channels” you are able to save, and earn in multiple ways. You can only unlock the three via signing up for ‘Vitality’. More on each those next.

1. Vitality Exercise

This one seems so easy when you begin and basically if you reach exercise goals each week you get rewarded. The minimum reward is basically 150 miles (R15 if converted to cash, but worth a coffee if you spend it as miles – the current flat white at Vida is R36, Caffe Mocha R43), but you can get up to 900 miles, my best being 450 to date (ie. three coffees, worth up to R129, technically). However, the big catch is that as you hit your goals each week, they up the ante and it’s harder to complete your weekly goal. For anyone with a little time, it’s pretty easy to make them each week, for at least the first 16-20 weeks, but it does get tough eventually! Add to that, being sick, or having work pressure, or Xmas time, or travelling overseas, or managing a newborn etc etc – and it can be testing to achieve the goals.

Essentially, if you were to do a decent 15-20 minute walk each day, you would easily be able to get 100 points a day, which in a wweek equates to 700 points. You will then probably fulfil your exercise goals for the first 30 weeks or so before you start needing to achieve 750 points in a week. For that, you need to get your heart rate up for more than 30 minutes – eg. walking isn’t going to cut it (unless hiking up a hill), and you will need to jog, or cycle, or swim (or tennis etc).

Why would you want to achieve these goals? There are two main reasons:

a) If you do, you get rewarded each week with Discovery Miles, which equates to a coffee, or some cash, and if you are luck on what they term the “game board” you can get a lot more miles. Let’s say the spectrum runs from 150 miles up to 900 miles – so R15 to R90. The trick is to build them up, and buy something worth R2,000 down the line, but we will get to that later.

b) If you do enough exercise in a year, and couple that with passing tests around your habits, BMI, cholesterol etc, then you can achieve Gold Status, which means you get even more money back from purchases, or discounts – and when those two are used in conjunction, it’s a powerful means of earning and saving. Again, more on that down below.

2. Vitality Drive

Like the above, if you pursue healthy driving behaviours, you will get rewarded. Again, there are some caveats, like paying money to get a vehicle tracker installed on your car, but once things are going well, you will more than make that money back. Currently, my car insurance (including home insurance) is about R400/m cheaper with a competitor than with Discovery Car & Home Insurance – I won’t migrate until their offering is much better, which should happen in 2024, as apparently the three year mark is key; I’ve only had car insurance for 2.5 years, as I was a loyal scooter driver for almost ten years!

However, the fuel rewards, and “good behaviour driving’ rewards in one month will exceed the extra R400/m that I am paying Discovery. Let’s say I spend R1,000 on fuel, and get R400 back for it, then drive well for four weeks, and get R200 back in that regard, then it is worth it. But, the key (I will say this multiple times on ths article and others) is the way you build up combinations of good decisions that Discovery incentivises you to do. So when you buy something with your Miles – let’s say a R1,000 Takealot voucher – with just Vitality Exercise in play, you will get it for R900 (10%) but with Vitality Drive as well, you can get it for R800 (20% off), and of couse, if you are thinking ahead, if you have Vitality Money (below) as well, then it’s 30% off.

So the wise man will do this: Get all three Vitality products, then earn Miles on all three and let them accumulate for months, then buy a giant voucher (maybe R10,000, for argument’s sake) at 30% off with those Miles, and they then have a R10,000 voucher, for “R7,000” – but it actually cost them nothing.

3. Vitality Money

For this, you need to sign up to Discovery Bank. There are a bunch of options, and as I was to learn the hard way, the free tier will do nothing for you – don’t bother! However, even on the lowest paid tier, you will reap some rewards. The sweet spot is the black card (I think about R400/m) and the purple tier (most pricey) is not worth it, unless you fly overseas like 2+ times a year. I landed on the Platinum tier, and am happy for now, while I transition away from FNB. It’s taking me a while as there are so many things to finish properly before migrating (Cellphone contract, SARS, plus others that take time, including getting a child’s passport), but that isn’t why we’re here…

As you can expect, the trick again (like with Drive and Exercise) is to behave well. Get rid of debt, save for retirement, spend wisely each week and month, and you get rewarded. I’m still early on in my journey, but am already getting 50% back in healthy food, which equates to about R1,200/m in cold hard cash, and another R600-800/m from other rewards. Of course, there is also the huge benefit of getting a pretty dismal % back on every card swipe. This is a huge deal as I think other banks are quite miserly on this one, and why not get a few hundred bob back each month just for doing something you would do anyways?

Initial Conclusion and Caveats

To make all the trouble listed above worth it, you really need to go “all in”. You will need to change banks, change car insurance, get a fitness watch/device (Fitbit, Apple, Garmin etc), stay somewhat fit (not massively), make a point of doing a weekly check in of five minutes or so on the app/s (to earn your miles, on the game board), and mostly: deal with the extra mental burden of thinking about this all. It really does affect you to think “have I achieved my exercise goal” every, single, day. I am happy to do it because it makes me healthier and more aware of my health; other folks I know really loathe it, and I totally get it.

Most of all though, if you grasp the concept of making a huge mission towards planting an avocado or lemon tree – buying it, digging a huge hole, fertiliser, compost, disease control, watering – for the first few months, and then reaping the fruit of that tree for 10 or 20 years, and you think that concept is a great idea, then jump in. If it’s not appealing, then seriously, do not even bother to begin, because it’s a lot of admin for 1-4 months.

6-9 months later: WAS DISCOVERY VITALITY WORTH IT?

The beauty of writing this almost a year later – in early March 2024 – is that I now have a much better idea of Discovery, its products, and the big question we see so much in search results (“Is Vitality worth it?”) And so, is it? My answer is, hilariously, just as before: it depends.

So let’s see what those things depend on. I am going to break this down into a few parts, and those are: what I learned in 2023, what I plan to do in 2024, what the alternatives are, and then should you got for it?

WHAT I LEARNED FROM DOING DISCOVERY VITALITY IN 2023

Essentially, I will give you the quick TLDR answer up front, and then say why: yes. It was worth it. Economically,

- I earned R15,600 in 2024. Though I only really started earning from May, as that was when I had capacity to really work the system. Context is having a baby, if that helps.

- I spent R3,228 on Discovery Bank fees. Bear in mind, I was paying a similar amount on FNB, so this has disappeared. FNB earned me eBucks, but it got to such a low point, that it was not worth it anymore. Hence the switch.

- I also spent R5,580 on Discovery Vitality. If I was single, this would be cheaper, and we don’t really benefit from the whole family being on it, especially a 1-2 year old who isn’t going to walk around with a smartwatch, even though he probably does 25,000 steps a day!

- So the quick maths there is: R6,826 income. Average of: R569/m.

- However, I want to do a monthly average on May to December, as like I said earlier, Jan-April weren’t the easiest. That total is R663/month – based on eight months.

- Lastly, as that figure is not life-changing, I want to mention that my best month last year gave me R2,262 back in cash, which I can take out as cash, or use to spend on various things.

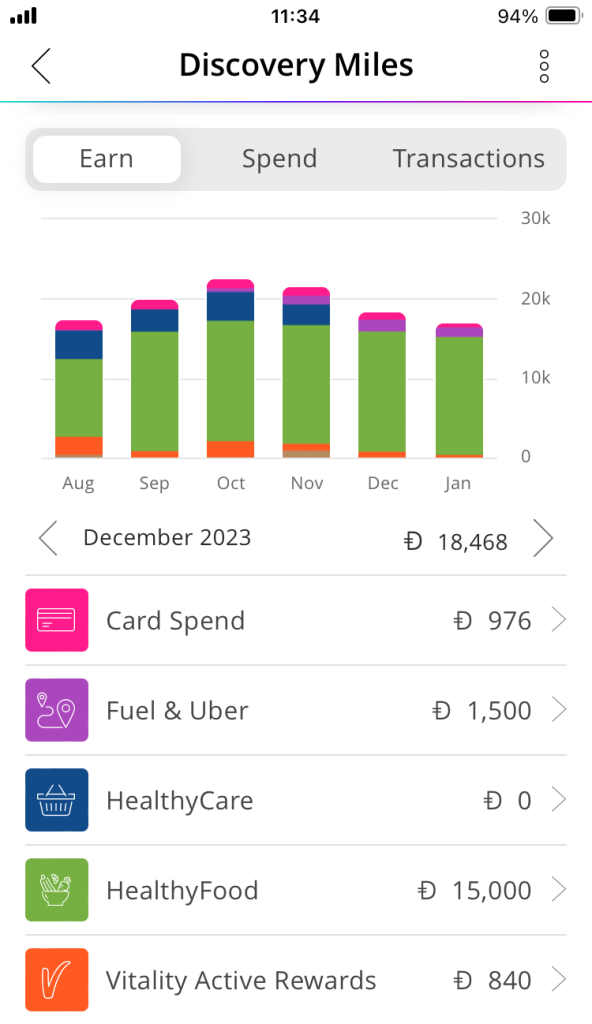

Here is a nice little snapshot of some proof.

WHAT I PLAN TO DO WITH THE WHOLE DISCOVERY SUITE IN 2024?

So this year the main goal is to finish with all the products. It took me a long time to find the time to go through the hassle of moving car and home insurance, and as I knew that once I have had continuous insurance for 3+ years (on my car/home) I could get a better deal, I delayed this a bit. So the 30-40 minutes invested in chatting with a guy on the phone has now happened, and then I took 10 minutes to photograph my car and license disc and upload that, and next is getting the vehicle tracking feature. This is certainly going to up my monthly earnings, and I am going to paste screen grabs on the progress of this in months to come.

Then, secondly, though I need to read the t’s and c’s, I might also use their investing/financial product as I already have Easy Equities, but I’ll have to do my homework. Anyone who has done an hour’s research into investing and such things knows that you really need to save on fees, which is why I keep away from financial advisors, and them taking their cut. That “little” 1% or 3% or what have you, ends up costing you more like 10-25% over 40 years. Not a wise decision.

Thirdly, I plan to move from the Discovery Bank Platinum suite, to the Black suite. I think the change is about an extra R150/m on card fees, but the extra earnings will surely be worth it. The plan is to do it in May/June, once I’ve completed a full year on Platinum. I do like ring-fencing things in years, for better data visualisation and year-on-year comparisons.

WHAT ALTERNATIVES ARE OUT THERE?

Well, as of writing this, I am not sure another bank can rival Discovery in terms of rewards. A few high earners I know swear by Investec, and that is likely because they have made it so much simpler for them. I thin the flat fee of R500/m and their list of benefits is smaller, and simpler, and for time-pressed folks, that is what they want. “Just give me my airport lounge access, and a flat white” I hear them say.

I signed up for Bank Zero, but feel like they need more time to polish up all their products before I engage with it. I don’t know if that will happen in 2024, and I doubt it for a user like me. As for the rest. I can’t see ABSA doing anything for consumers, ever. Standard Bank seems on a par with FNB. Tyme Bank is progressive but probably more focused on expanding globally. Capitec isn’t interested in my earning bracket (yet!). Nedbank I don’t think has the personality to innovate… let’s hope I am wrong. And, I can’t think of any others, but I do wish HSBC returns to South Africa.

SHOULD YOU GO FOR DISCOVERY VITALITY IN 2024?

At this stage, half my answer is that it’s very much as I said last year in the first part of this article, and its pros and cons on joining. But also, the second half of the answer is that in that time frame, though they have improved the offering in slight ways, the things that have left – or gotten worse – is greater than the improvements. Here are some examples:

- When I began, a smoothie was R20, or 200 miles. It changed to R25 or 250 miles late last year, and then became R30 or 300 miles this March 2024. Considering my income, or way of earning miles didn’t go up with such pace, this is a little unfair.

- Last year, until June I think, you could get ‘the iPhone benefit‘ – a sort of “free” phone (a luxury one at that), if you achieve goals etc. At about R20,000 value, this is a huge thing, and now taken away, means I miss out on perhaps something like R10-12,000 of value in a two year cycle, considering I am not going to achieve 40-50% of my goals. Let’s be honest, I don’t want to be a slave to getting 10,000 steps daily, at any cost.

- I am still a bit confused as to the maths behind it, but from the little I can tell, the smartwatch benefit has also dropped. I think my first smartwatch was fully funded (my memory tells me 75%) upfront, based on ticking all the right boxes, and some exercise goals accomplished. This time round I got 50% off upfront, and I think there is a chance I can get the rest of the 50% off by completing goals, but it’s not certain. It was certainly unclear. I went for a cheap Garmin anyway, so it’s not going to bother me.

- You may have seen my screengrab above and noticed something – the blue disappears for December and January, and this is because there was an error on Clicks and their “Health” products not counting. It was an error in their side and I got 3-4 months points in a bumper February 2024. Why do I make mention of this? Because the error means I had to jump on their WhatsApp hotline and chat through it with an agent for 10-15minutes of my life. It was worth it as I earned another R1,200 or so because of it, but if too much of this involves my time, it becomes too much. In a similar vein, my bank fees have been wrong once before, and I had to jump on a call, and if you are on the line for more than 5 minutes, you start questioning the process, and valuing your time more. Again, this is still better than FNB (who are great, for the record), and so it’s part and parcel of any bank admin.

- Next, I used Virgin Active for a year, and the saving here of ~R750/m was great for my knee rehab, and swimming. It ends now in April, and means I lose out on those weekly smoothies, and lovely swims. However, I did spend R50 in fuel a week (I’d guess) to get there and back, and am happily returning to the ocean and mountains of Cape Town for a bit.

That benefit, much like airport lounges, and cheap flights, really are an individual thing, and if I fly this year, I’ll be so glad to be on Discovery, if not, then it’s another reason to not bother switching banks and medical aids.

Check back in 3-4 months time and see how March to June progresses, where I should start seeing more Miles earned per month. The goal: to hit R3,000 (30,000 miles) in a month. Wish me luck.

————————————————————————————————————-

July 2024, A Miles Update

It’s been 3-4 months now, and here is the update since then, with five more months of data. I’ll add some thoughts below.

First, hitting around R2,000/m consistently is great for two reasons:

One: It makes the whole Discovery Ecosystem and Vitality worth it, and

Two: It now involves almost no work. As everything is set up, it’s pretty painless to just let it accumulate points each week.

Then, I’ve subsequently got into Padel and other sports and started benefitting from the gear discount. I’ve adopted Discovery/Vitality Drive, and have so far earned back: R250, R370, R420, and now R560 each month – and as someone working from home, it’s hard to do many kilometres. But one long trip up the coast and I could very easily get the maximum reward of about R1,250 (policy dependant).

You might notice the annoying bocks of blue are every 3-4 months, this is because either Clicks or Vitality struggle to reward the miles each month, and so you need to nag them. Either that, or just be patient. As I let my miles accumulate for 4-6 months anyway, it doesn’t bother me.

My last parting thought for this quarter is that our family got ill for six weeks, and with other factors of a young family, my exercise hasn’t been what it should – so all those bar graphs could be a little higher. I have a good feeling for the rest of the year though, so let’s see how this all looks come December.

————————————————————————————————————

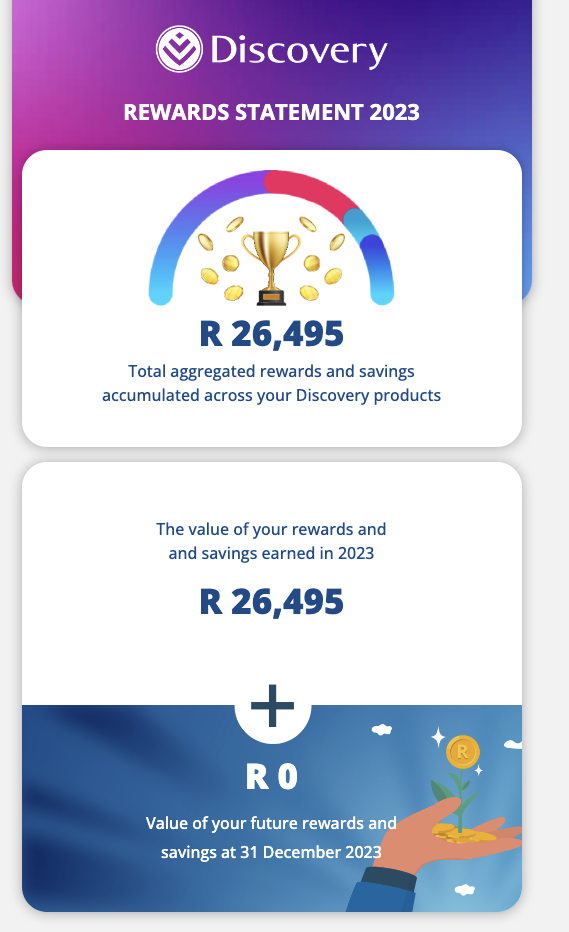

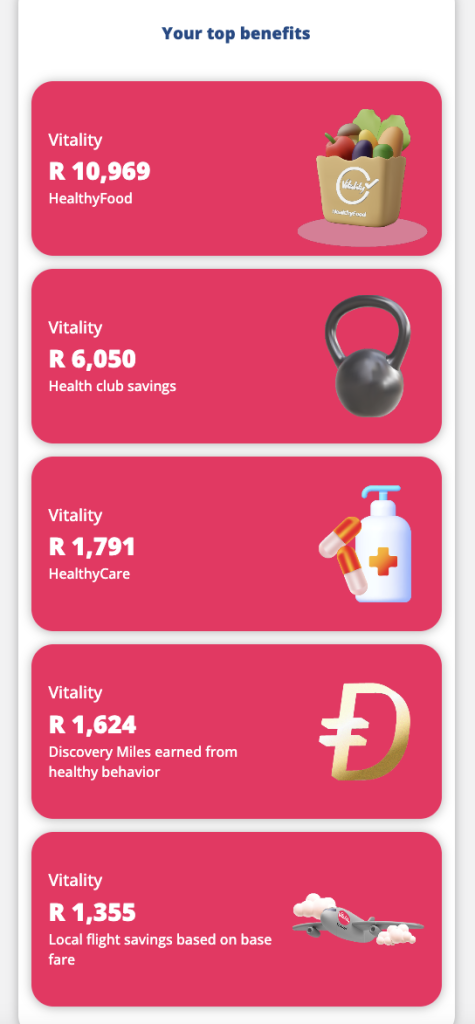

Minor Update: To see how I fared last year, Vitality just sent me (mid-March 2024) a snapshot of my earnings for last year. It summarises the main savings and benefits with a Rand value.